RENEWABLE ENERGY ASSETS FINANCING

ABOUT US

Rylands & Hamilton(“RH”) provides Debt Financing to Renewable Energy Assets.

A firm imbued with a singular focus and rich experience in Renewable Energy, RH has been providing Financial Advisory Services exclusively to the Renewable Energy sector in India since 2012.

The Firm specializes in Acquisitions, Joint Ventures, Structured Tax Equity and Project Finance transactions and typically represents Strategic Investors in such transactions.

WHAT SETS RH APART?

At RH, We are passionate about Renewable Energy and believe in the importance of its growth. Forward looking, industry savvy. We understand the renewable energy industry and strive to predict strategic trends. This is demonstrated by an unparalleled track record over the last years.

Focus:

Renewable energy sector is RH’s prime sole focus. Multi-faceted solid track record. Renewable energy Project Financing is a relatively young industry, where transaction structures continue to evolve. Due to the unique nature of risks in most renewable energy financings, transactions need to be constructed with a fine balance of Risk Allocation. With deep sector experience, which includes leading roles in large-scale Wind and Solar Power transactions, RH offers meaningful insight on maintaining this fine balance.

Services from M&A and Joint Venture Advisory to Project Finance and Tax Equity structuring, each of RH’s service offerings are underpinned by core competencies. With solid experience in the energy markets and financing execution, RH brings a comprehensive perspective in each of the service offerings.

Since 2012, RH has been working with a number of large Institutional Investors to make them aware of the risks and benefits of investing in the Debt of Projects within the renewable energy sector given the long dated nature of the assets and the underlying cash flows. Given the substantial transaction costs involved with direct issuance, RH has been established as a conduit to provide attractive long term debt financing at competitive levels and with sensible transaction costs.

Services

Project Finance ans Tax Equity

- Identify markets

- Optimize structure

- Strategize market approach

- Assist in execution

Strategy Advisory

- Identify critical emerging issues

- Position as "first mover"

- Risk diversification strategies

- Cross-border joint ventures

Deal Facilitation

- Acquisitions

- Partnerships

- Joint ventures

RH core competencies

Project Finance ans Tax Equity

- Financing strategy

- Transaction structuring

- Transaction execution

- Restructuring

Deep Knowledge of Markets

- Renewable energy industry

- Bank market

- Institution investor market

- Tax investor market

Significant Industry Network

- Developers seeking capital

- Investors seeking capital and

partnering opportunity

partnering opportunity

SEGMENTS :

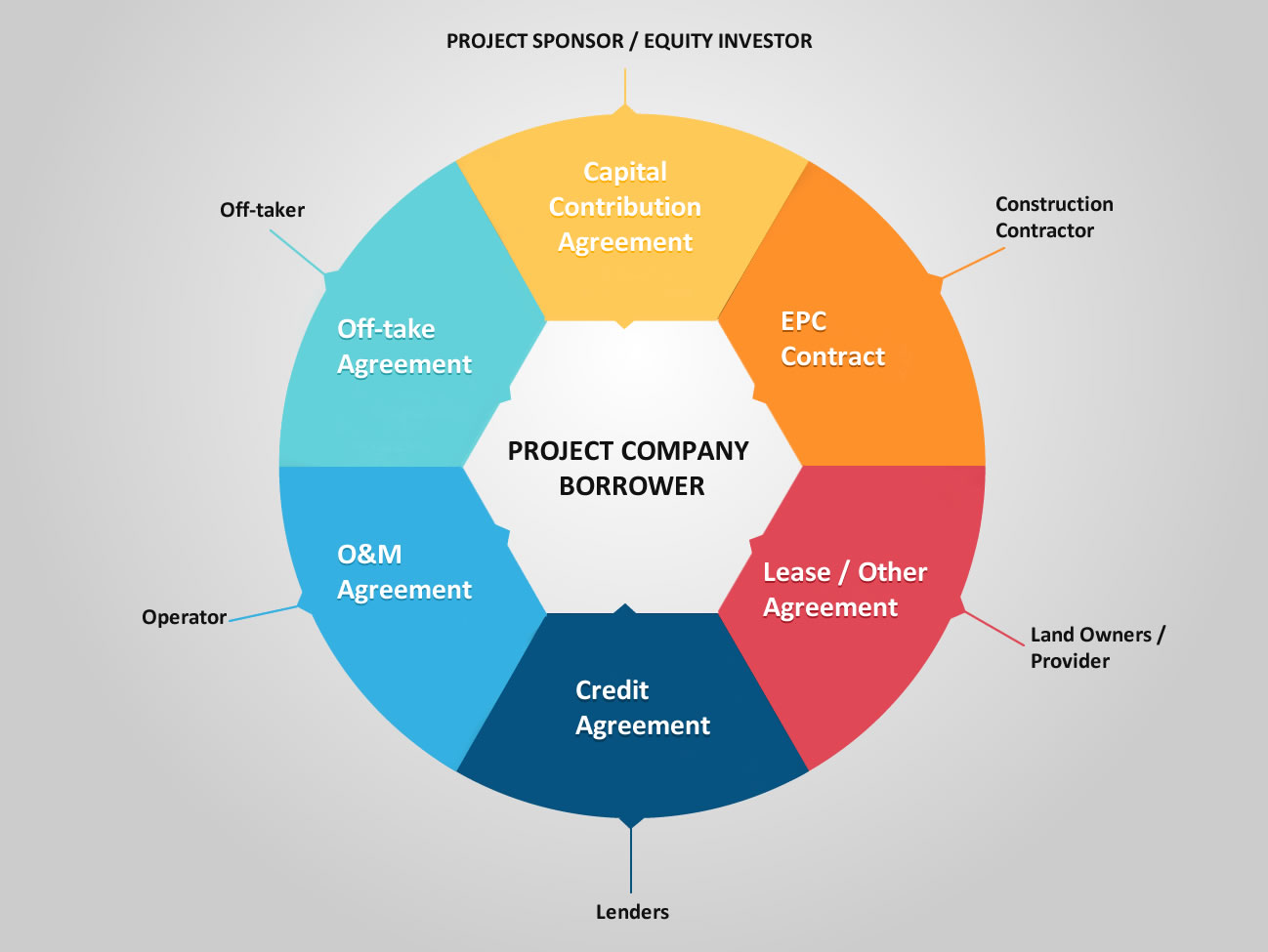

RH works with Renewable Developers, EPC contractors and Equity Sponsors to support Renewable Energy by providing Construction Finance.

We can provide finance of up to 100% of the Loan-To-Cost (LTC) for shovel ready assets.

Our finance offering is composed of Long Term Senior Debt (up to 25 years), thereby eliminating any refinancing risk and other additional associated costs. Short term Mezzanine finance (E.g. Equity-Bridge) can also be provided if required.

RH provides financing solutions with innovative structures and can offer Debt of up to $100 million per project. RH offers long term finance to match underlying regulatory tariffs.

RH's long term financing facilities negate future refinancing risk and associated costs for the borrower.

The financing facilities can be structured with either a fixed or Inflation-linked coupon and with Fixed and Floating charges over the assets.

RH is now able to provide Landowners who have leased their land to renewable operators the ability to monetise the future value of the long term lease payments they will receive.

The landowner retains Ownership of their land and receives a upfront lump sum that can be used as they so wish.

The loan facility that RH provides matches the term of the underlying land lease and is secured against the Rental Incomes.

RH has Loan Arranger partner companies, in order to identify potential renewable energy assets as suitable investments for RH and as Loans Administrator in relation to each loan that RH makes.

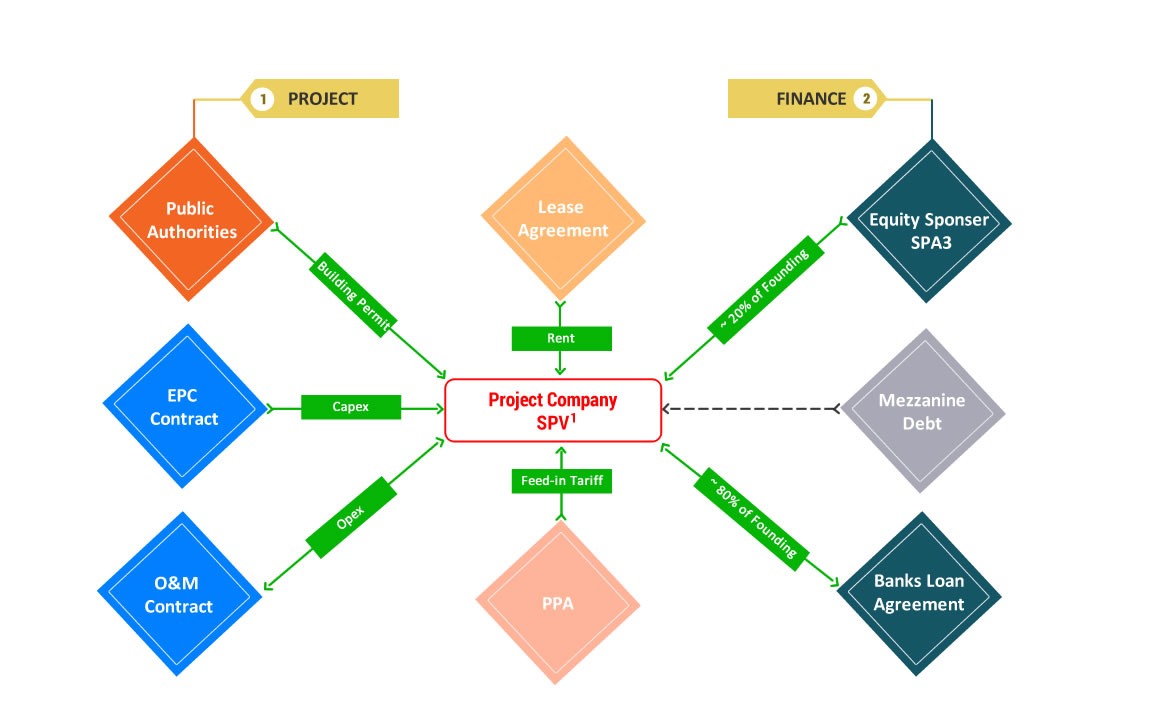

FINANCING STRUCTURES :

Here are some of the more common Structures of financing Renewable Energy project.

They vary in the type of Participants, Source of financing and Allocation of benefits

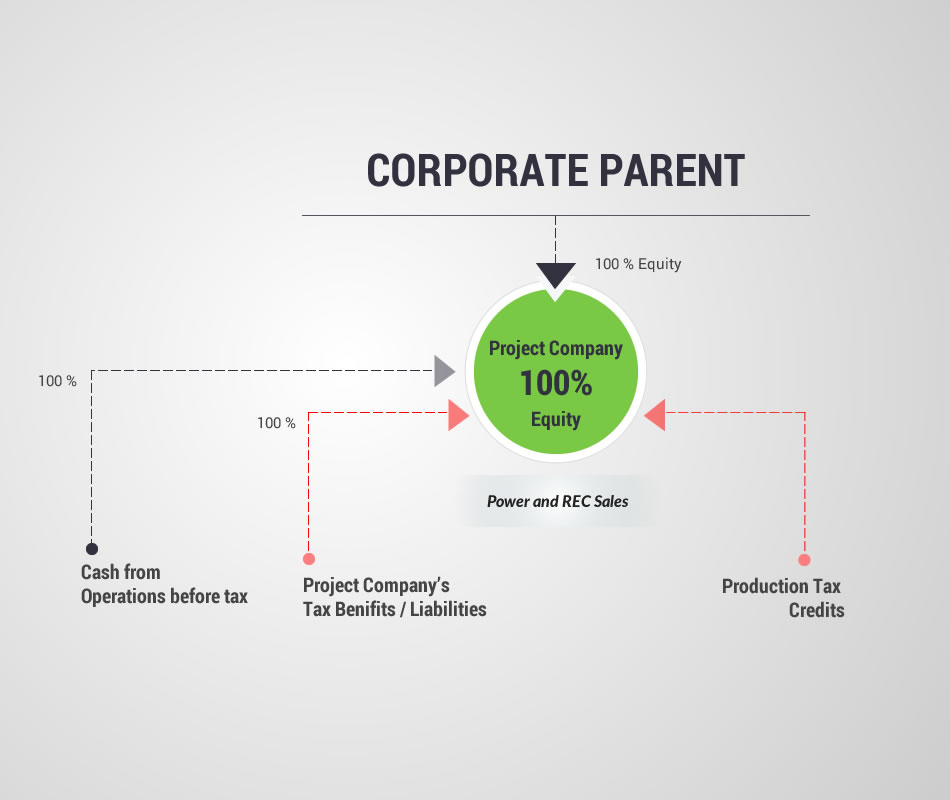

One Corporation develops the project and finances all costs. There are no other Investors or Lenders involved.

The project may be set up as a subsidiary of the Corporate Parent. However, with 100% ownership, the subsidiary would have to be consolidated into the parent's Financial Accounts.

Naturally, the corporation reaps all the benefits of the project.

The Corporate Parent must have sufficient capacity for tax credits and benefits to be of use.

In the renewable energy sector, this is structure is rare and only used by Utility Companies themselves.

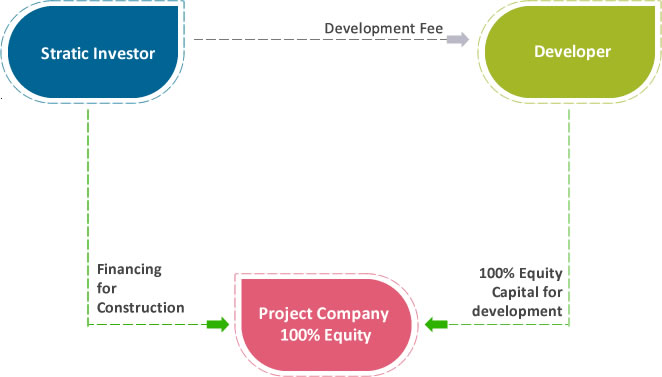

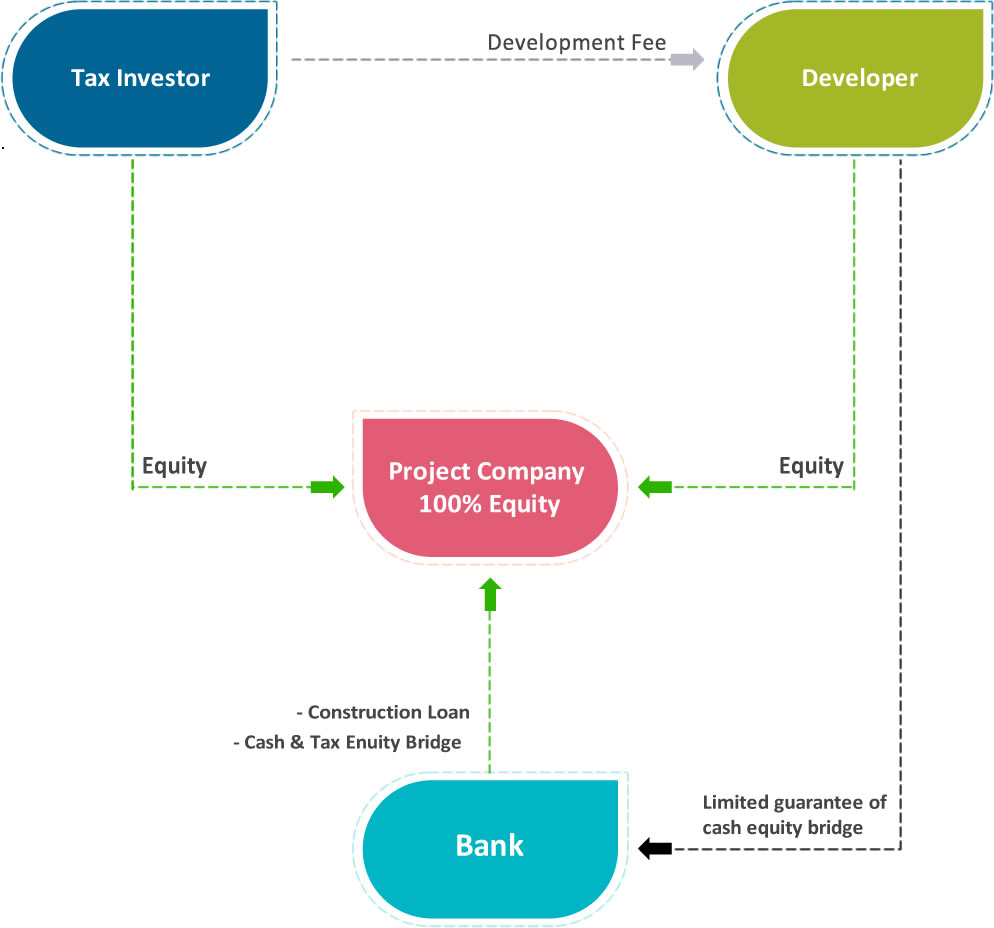

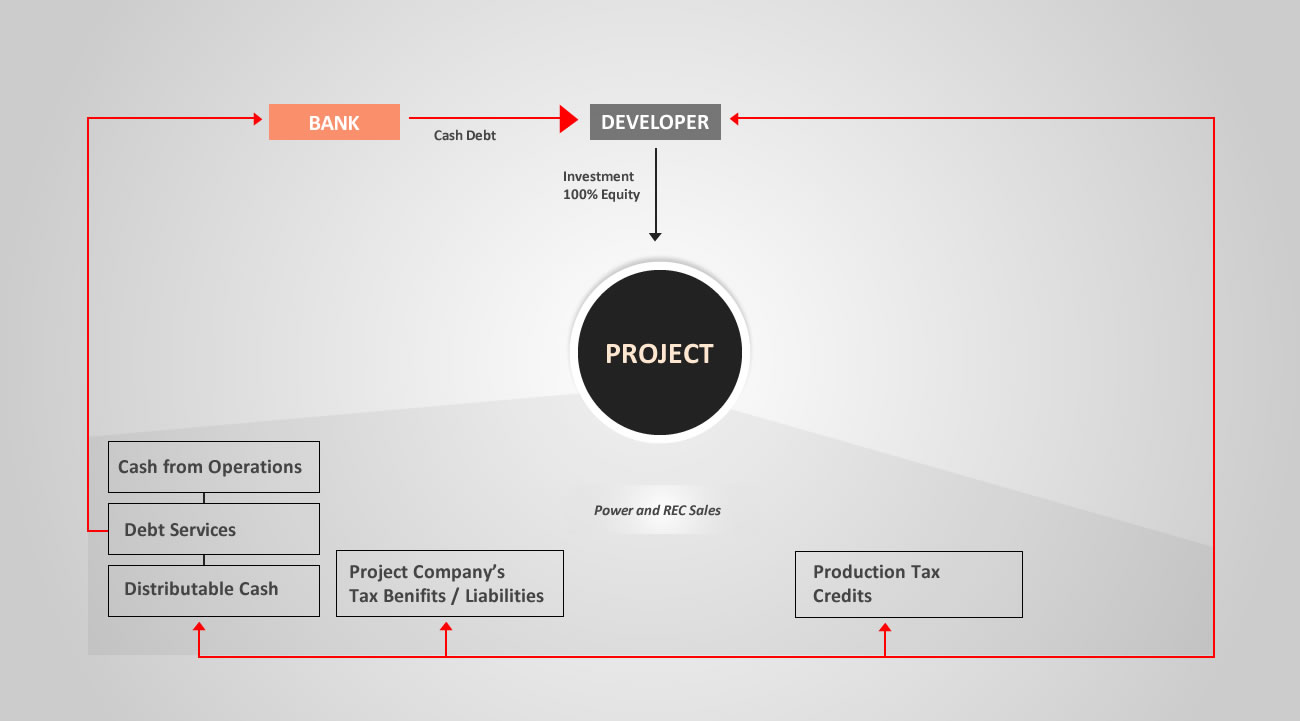

The Developer acquires Lease and Land rights, Permits, Interconnection Agreements, Power Purchase Agreements(PPA's) and any Renewable Certificates(RECs) or Feed-in-Tariffs.

The Developer sells the developed project to a Strategic Investor and receives a Development Fee from the Investor.

The Strategic Investor (possibly a Utility Company) constructs the project on its Balance Sheet OR arranges Bridge Finance for the construction. The Strategic Investor owns and operates the plant. The Developer's risk is limited to the Development Capital.

The Developer seeks Bridge Financing from Lenders:

Construction Loan: Bank is repaid in full at completion of construction. Alternatively, Bridge is converted into Long-Term loan.

Cash Equity Bridge:Bank is repaid at completion of construction with funds from Sponsor. Developer may provide limited guarantee for Cash Equity.

Tax Equity Bridge: Bank is repaid at completion of construction with funds from Tax Investor, who will only come in once the plant produces tax credits.

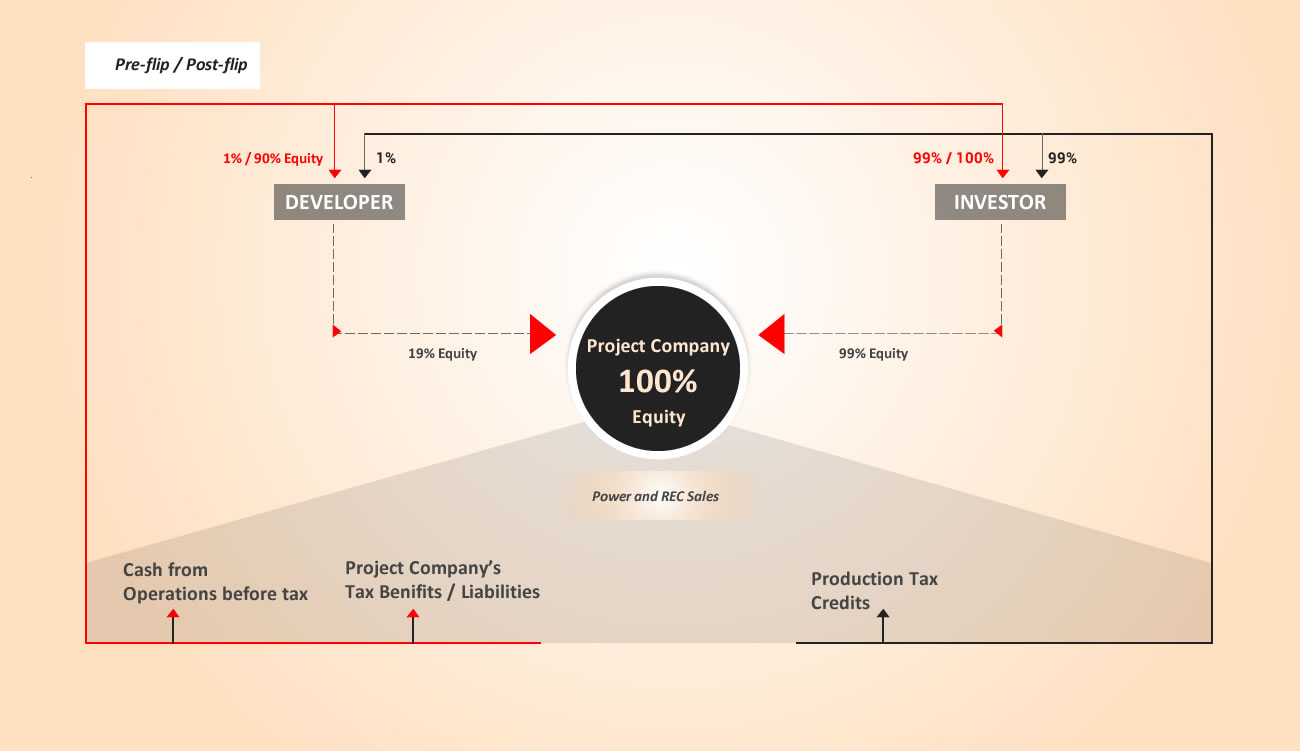

The Investor contributes almost all of the Equity and receives a Pro-Rata percentage of the cash and Tax benefits prior to a flip in Allocation.

At a given level of IRR (Internal Rate of Return), the ownership flips back to the Developer, after which most of the cash and Tax benefits are allocated to the Developer.

Only the production Tax credits will continue to go to the Tax Investor even after the "Flip".

If the Investor is a Tax Investor rather than a Strategic Investor, the Pre-Flip allocation may not be Pro-Rata, and all tax benefits may go to the Investor instead.

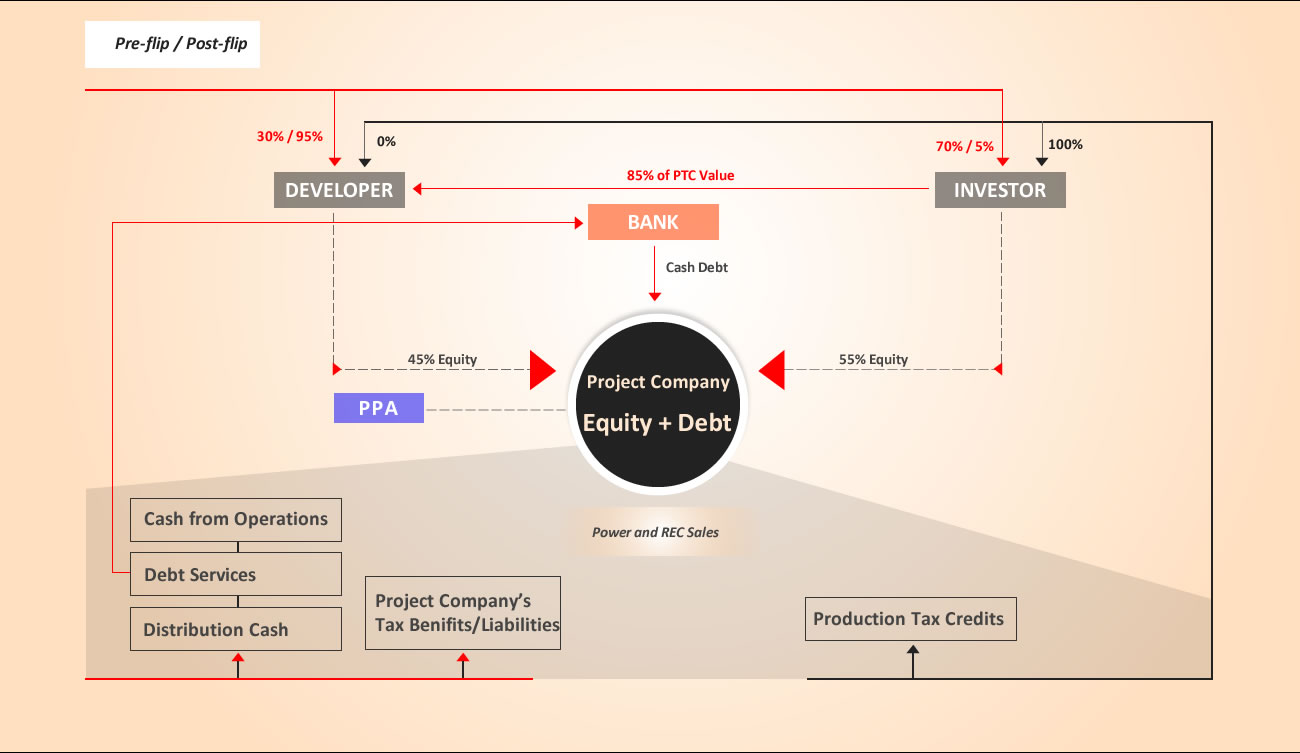

This is the most common Project Finance structure.

The Tax Investor makes contributions before production begins, though a portion may be deferred until the project receives production Tax Credits, which are initially allocated to the Tax Investor, though a high percentage is paid to the Developer as an Equity contribution. This serves as a claw-back should the project not perform.

The leverage is at project level with Long-Term debt of up to 25 years, based on the PPA (Power Purchase Agreement).

This structure also includes a Return-Based Flip in the allocations.

As the term for the production tax credits is usually, an additional loan may be secured against those flows.

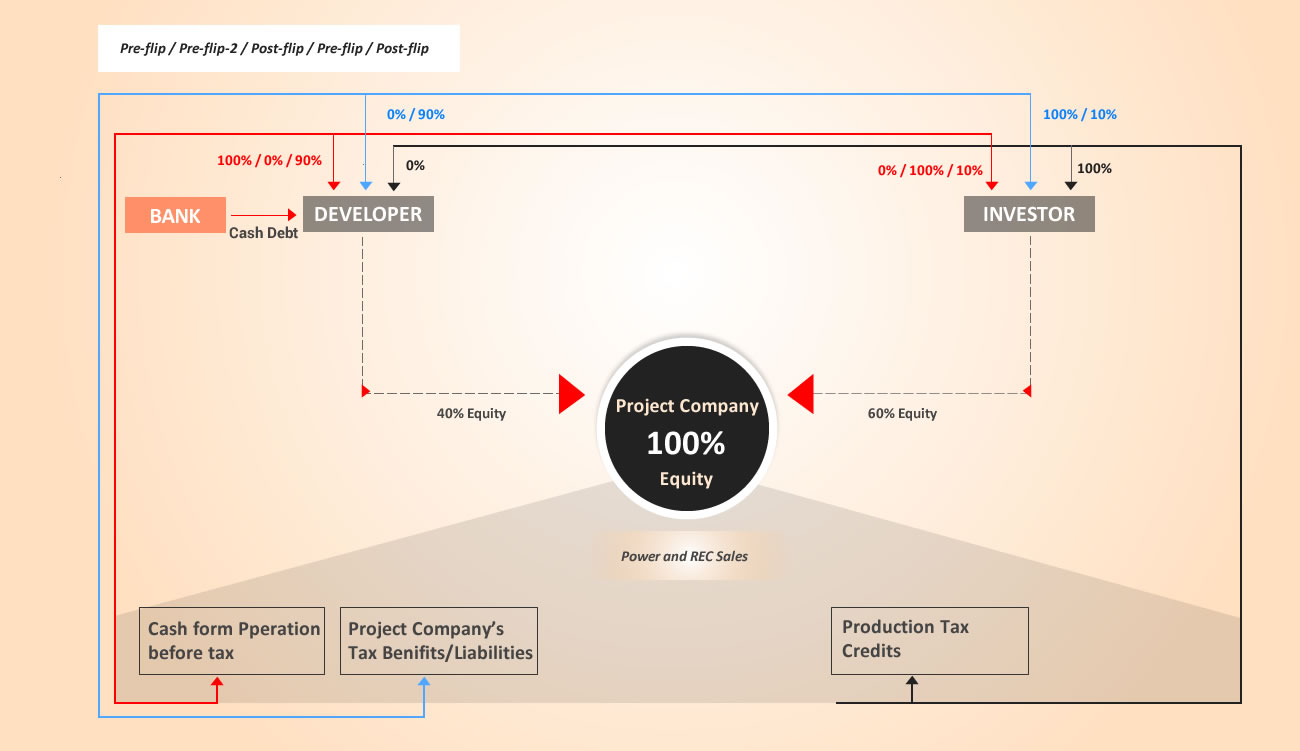

Similar to the Investor-Ownership-Flip structure. However, the developer is leveraging its Equity stake in the project using Debt Financing.

The Tax Investor commits Equity upfront.

Pre-Flip: Initially, 100% of cash goes to the Developer until Return of Investment (similar to a Development Fee). Then 100% goes to the Investor.

Post-Flip: After the Investor's pre-agreed IRR (typically 8% - 12% depending on Project Risks) is reached Ownership and Cash flow allocations go back to the Developer, including most of the Tax benefits.

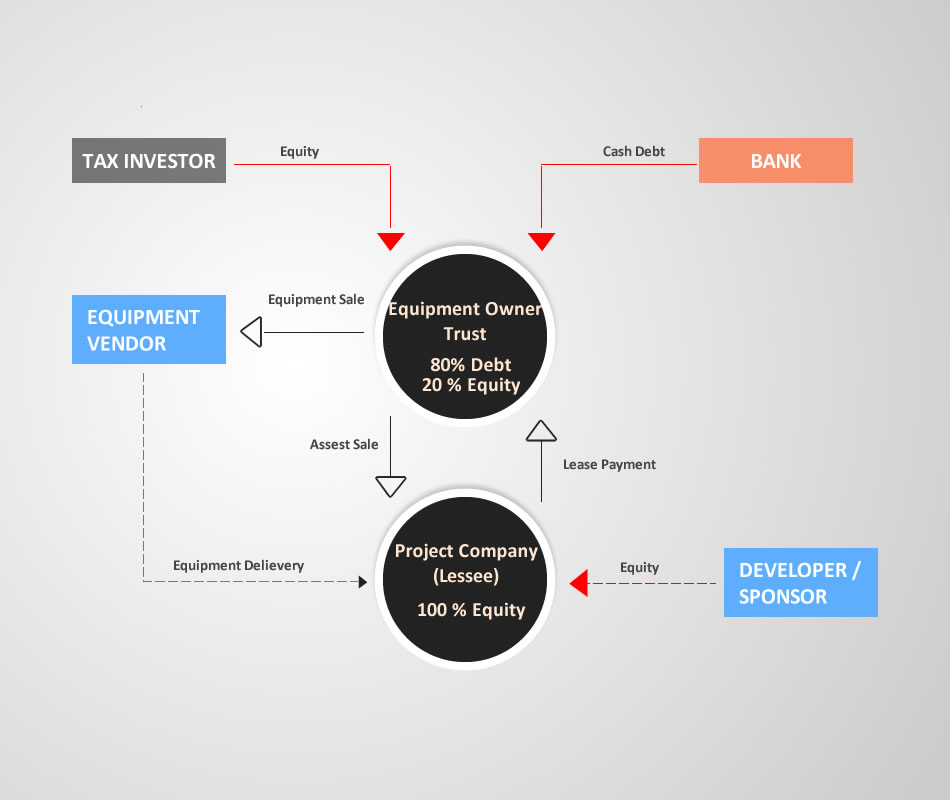

Construction is funded by Sponsor Equity and a Construction Loan. Once constructed, the Sponsor sells the Project to the Investors that have formed a TRUST and immediately leases it back.

The Developer repays the construction loan from the sale proceeds. The Trust is financed with Cash Equity and a Non-Recourse Term Debt. Lease payments are likely to be assigned to a Lender. For tax purposes, a minimum of 20% equity is usually required.

Leasing generates a "Time value of money" cost saving achieved by Deferring Tax payments. It also improves Cash Flow. If set up as Operating Lease, the lease may only be for 5 years with the option to re-lease.

Construction is funded by Sponsor Equity and a Construction Loan. Once constructed, the Sponsor sells the Project to the Investors that have formed a TRUST and immediately leases it back.

The Developer repays the construction loan from the sale proceeds. The Trust is financed with Cash Equity and a Non-Recourse Term Debt. Lease payments are likely to be assigned to a Lender. For tax purposes, a minimum of 20% equity is usually required.

Leasing generates a "Time value of money" cost saving achieved by Deferring Tax payments. It also improves Cash Flow.

If set up as Operating Lease, the lease may only be for 5 years with the option to re-lease.

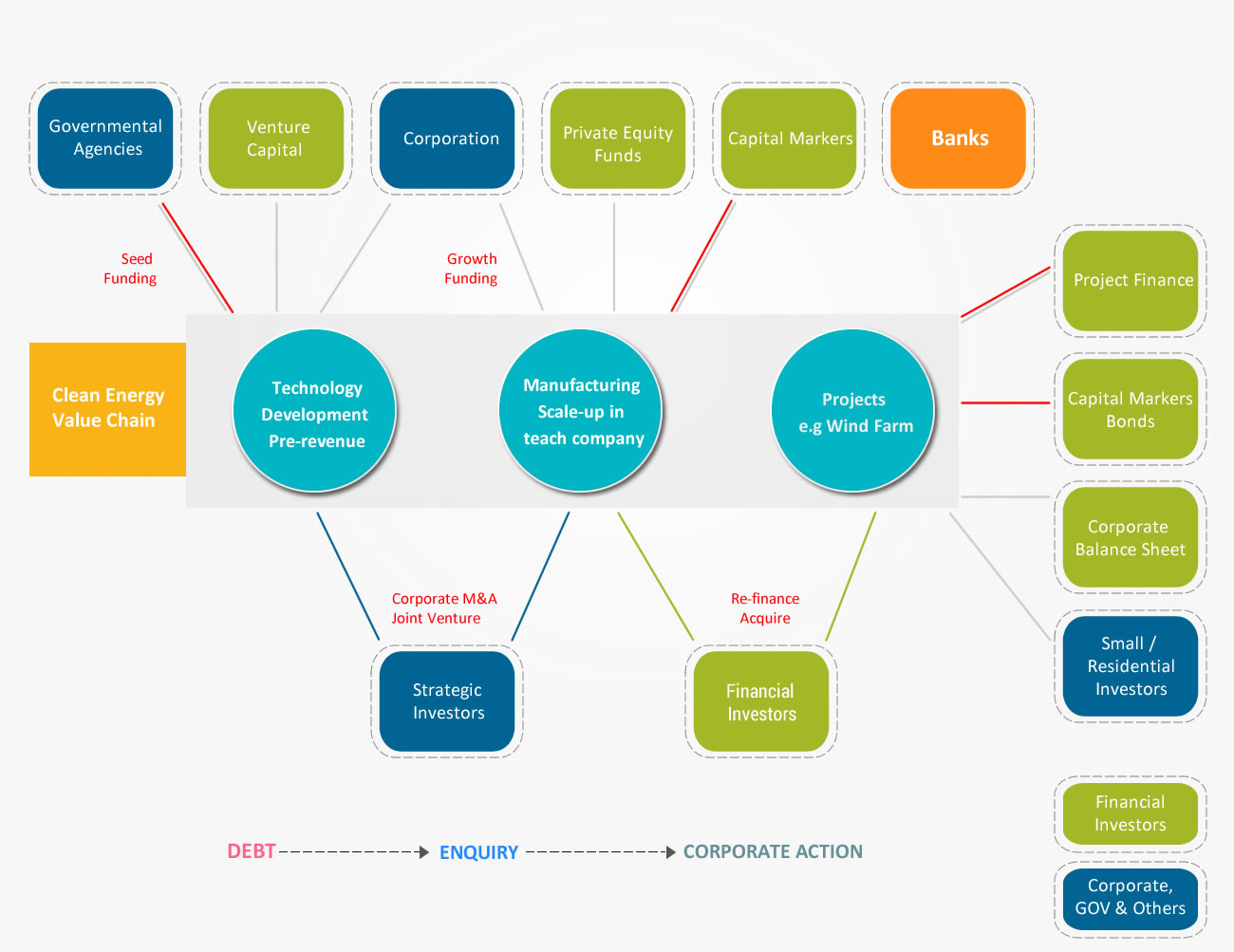

THE VALUE CHAIN OF INVESTMENT IN CLEAN ENERGY

There are Four different types of Investment opportunities along the Technology Value Chain:

- Funding of Research & Development of new Technologies Pre-Revenue;

- Investment in Companies to scale up manufacturing of already developed technologies;

- Development and construction of Renewable Power Plants (Renewable Assets);

- Corporate Actions including M&A activities and Refinancing.

Most of the Seed and Early Stage Funding in clean energy is provided by Governmental Agencies, Research Bodies and Corporations with a sufficient Balance Sheet such as Utility companies. Governmental support is mostly in the form of a grant (that does not have to be paid back), sometimes requiring matching funds from Private Investors. There is also Venture Capital(VC) money at this stage.

With Technology risks significantly lower, but Funding requirements higher, scaling up the manufacturing can only be financed by Larger companies, Private Equity funds and by Raising capital in the Public stock or Bond markets. At this stage, Debt may be available from Banks as well.

There have been a number of stock market entrances already from Solar and Energy-Efficiency Companies. These "Exits" either through an IPO or acquisition are important if Investors are going to keep funding Energy-Technology Ventures.

Depending on the size of the Installation, New Assets are financed by Private Investors (Small projects like Rooftop Solar Panels), Corporation's Balance Sheets, Project Finance or by issuing Bonds.

A significant amount is invested in Corporate Actions including Private-Equity Buy-Outs, corporate M&As, as well as Acquisitions and Re-Finance of Renewable Energy Assets.